Inflation and Electricity Price Assumptions

Dr Chris Jardine explains how to calculate your financial returns.

CALCULATING YOUR FINANCIAL RETURNS

When we quote for a solar PV system, we also provide some financial information predicting the likely returns from your system. We estimate the total amount of monetary benefits you will receive, either directly from the Feed-in Tariff (FiT), or as savings on your electricity bill. We also use this to calculate an internal rate of return, which is the interest rate you would need to receive from a bank account to receive the same financial benefit from the same input of capital.

However, there are two key assumptions that must be made for these predictions. First, the Feed-in Tariff is inflation linked, so the p/kWh generated that you receive stays the same in real terms (goes up in absolute terms) for the next 25 years. Second, we expect the price of electricity to go up over the next 25 years, so we must also make an estimate here to determine how much we expect you to save off of your bills in the long term.

The return on investment that is quoted is highly dependent on these two assumptions. We are extremely aware of other solar companies making their returns look amazing by being, shall we say, a little over-optimistic in their assumptions.

For example, a 4kWp system selling at £10,000 gives a rate of return on investment of 13.8% using our assumptions. This is what we tell our customers. If, however, inflation was assumed to be 4% and electricity price rise at 5% then those returns would have appeared to be a more impressive been 15.8%. sBelow we show the assumptions that we make, and why we use the values that we do. As ever, we aim to be sensibly cautious about our assumptions – we would much rather you were pleasantly surprised when your system exceeds our predictions, than for you to be disappointed in performance because a supplier has overstated the financial case.

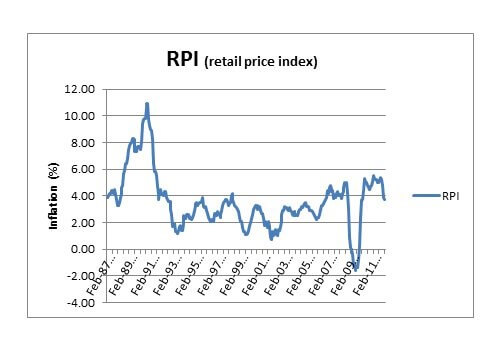

Recently, RPI has been running at about 5% per year. A longer term view of RPI, ignoring the very high values seen in the late 80s, has an average value of ca. 3.0%.

In trying to predict inflation for the next 20 years, Joju Solar have taken the cautious long-term approach and adopted a value of 3%.

ELECTRICITY PRICE RISES

Predicting future electricity price rises is notoriously difficult, and energy economists the world over would find it difficult to predict prices 25 years into the future with any accuracy. Nonetheless, we do have some idea of what the future looks like, and can say the following with some certainty:

Electricity prices will rise strongly over the coming years because:

Increased wholesale prices of gas used for electricity generation, as it is sources from increasingly far away (and potentially volatile) locations. International gas price is also linked to the price of oil, so price rises caused by peak oil may also start to play out through related markets such as electricity.

The need to replace existing generation capacity – we have about 20GW of nuclear and coal capacity due to shut over the next 10 years •Need to install high volumes of renewables to meet government and EU targets, incentivised both by the Renewables Obligation and the FiT itself

The need to fund energy efficiency improvements to reduce CO2 emissions

The cost of wholesale gas price is virtually impossible to predict. But the effects of policy are more certain and have been studied by the Department of Energy and Climate Change. They predict that the price per unit of electricity will increase by 33% in the residential sector and 43% in the commercial sector between 2009 and 2020. These are increases in real terms, and do not include inflation.

Joju Solar is therefore assuming electricity price rises of 2.9% per annum for residential properties and 3.6% per annum commercially.

Whilst these values may seem high, it is important to note that these are price increases due to policy only, and do not account for any increases in the wholesale price of gas that may arise. This has been the key driver of rising electricity prices for the last 10 years and we expect this trend to continue as well. However, because this cannot be predicted accurately, we are deliberately excluding this factor from our assumptions.

Sorry, the comment form is closed at this time.